|

talksatellite EMEA |

.gif) |

||||||||||||||||||||||||||||

Daily news |

Satellite Capacity

Pricing Declines Slow, But Price Pressure

Expected To Increase With New Supply Entering

Service In 2023 30 November 2020 In its latest research

titled, “FSS Capacity Pricing Trends,”

Euroconsult, reported that the dramatic pricing

declines of the past five years have slowed as a

result of notable slowdowns in new capacity

supply additions. However, intense pricing

pressure is expected to return in advance of new

capacity coming online in the 2022-23 timeframe. Over the past five years,

average capacity pricing levels in video markets

have dropped 30 percent in aggregate, while data

markets have experienced 60 percent declines.

While pricing is beginning to stabilize, the

previously strong mobility market is now seeing

pricing erosion in the short term, due to the

COVID-19 pandemic and its impact on global

travel. “We are seeing a mixed

landscape in current pricing trends,” said Brent

Prokosh, Senior Affiliate Consultant at

Euroconsult and author of the report.

“Despite the generalized pricing declines

globally, , strong demand for HTS capacity in

places such as North America and Southeast Asia

has led to regional shortages, alleviating

pressure in the short-term. While fewer regions

have reported sharply declining capacity pricing

levels, more challenging competitive

environments are reported for Latin America and

the Russia & CIS regions. Further, at key

orbital hotspots, Direct to Home (DTH)

television platform pricing has also been

notably resilient.” While DTH pricing of up to

$8,000/MHz/month is still in effect in some

locations, many platforms have sought to reduce

their commitments through lower volume and/or

shorter-term renewals. On the lower end,

capacity pricing ranges have remained relatively

stable over the past year, with $600/MHz/month

for regular and less than $100/Mbps/month for

large-volume long-term HTS capacity leases still

prevailing.

In its 3rd annual edition

of the report on satellite capacity pricing

trends, Euroconsult provides an analysis of the

structural trends impacting the industry and

delves into regional pricing for nine different

parts of the world. The analysis is based on an

expansive database of more than 2,000 capacity

pricing contracts and includes roughly 100 new

price points derived from more than a dozen

interviews and continuous desk research

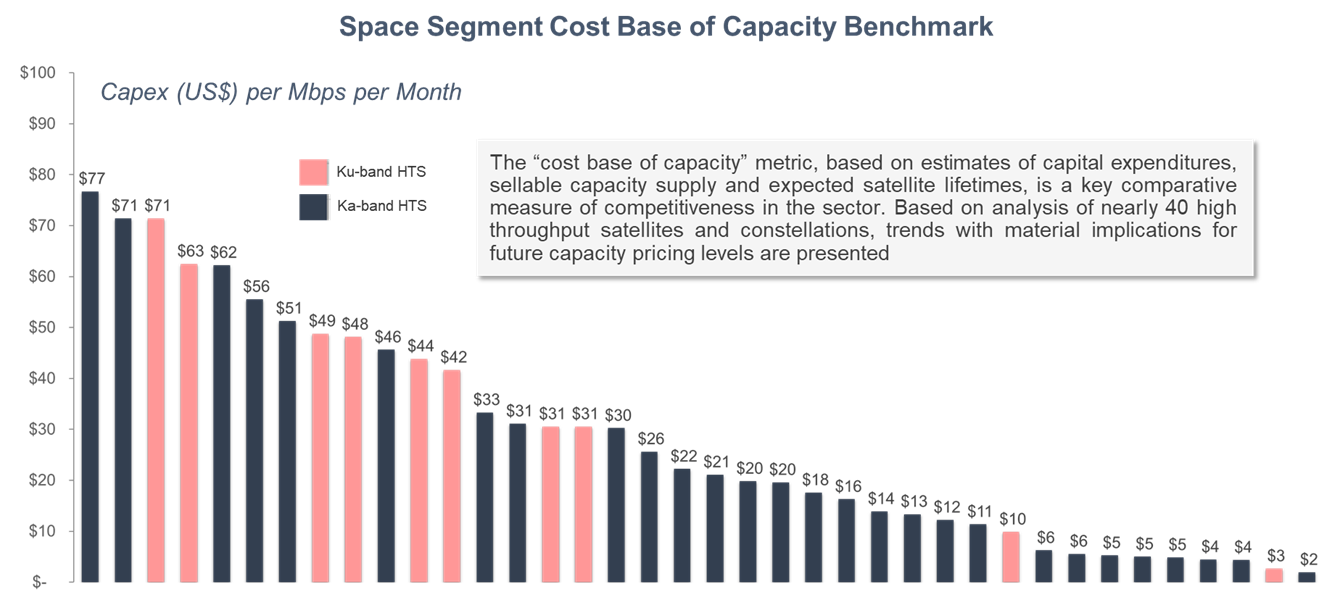

conducted over the past 12 months. It includes capacity supply

fill rates and case studies on the cost base of

satellite capacity. It also breaks out pricing

trends by spectrum and type of service and

includes an overview of milsatcom and mobility

pricing. Additionally, for the first time, this

year’s edition of “FSS Capacity Pricing Trends”

includes a section on in-orbit life extension

services. It also provides an analysis of the

cost base of capacity for nearly 40 HTS systems,

including all major Very High Throughput

Satellite (VHTS) systems and Non-Geostationary

Orbit (NGSO) broadband constellations. The research projects that

HTS fill rates, which are comparatively lower

than regular capacity, are expected to drop from

50 percent as of 2020, to below 20 percent by

2023 with new capacity expected to come on line

in that time frame. This oversupply will put

further pressure on capacity pricing. As a

result, Euroconsult projects that operators will

seek to drive utilization of new capacity by

testing the price elasticity of demand. “Another way that operators

are responding to oversupply and pricing erosion

is by adopting vertical integration strategies,”

said Prokosh. “This has the potential to provide

them with a higher degree of control over

pricing conditions. It is an especially relevant

trend, given expectations that competition will

continue driving the benefits of lower cost base

of capacity towards end user services as opposed

to the tradition FSS operator wholesale lease

model.”

|

|

|||||||||||||||||||||||||||

|

|

|

|||||||||||||||||||||||||||